The Complexity of Revenue Recognition in China Just Got Worse (Part II)

The Impact of the Coming Rule Changes under IFRS and US GAAP adds to the Already Complex Environment for a Foreign Firm doing Business in China

Part II of a Two Part Series

Jean Kester, Partner, LehmanBrown International Accountants, April 2015

As noted in Part I of this Two Part Series, on May 28, 2014, the International Accounting Standards Board (IASB) and the Financial Accounting Standards Board (FASB) jointly developed and issued a new revenue recognition standard that will supersede most current revenue recognition rules under both IFRS and US GAAP. This standard is – Revenue From Contracts with Customers Topic 606 under US GAAP and IFRS 15 under IFRS standards.

The effect of these changes on entities operating both in China and abroad will vary, and some may find the new standard brings benefits to financial reporting as well as significant changes in the way the entities recognize revenue. As the upcoming changes in revenue recognition and the changes many entities will need to make to comply with the new standard are expected to impact many areas of an entity, including financial reporting, business operations, IT and controls systems development and have potential tax implications as well, companies are beginning their implementation plans, which begins with an analysis of how the standard will affect them. An implementation will vary from entity to entity, depending on the breadth and depth of impact expected.

In Part II of our two part series on the change in the revenue recognition standard, we will examine suggestions for how to transition to compliance with the new accounting standard.

Set up a project team and conduct an impact analysis

Assign a team leader or team the responsibility to evaluate how the changes to the new revenue recognition standard will impact on how your company accounts for existing revenue and the results of operations, including evaluating how the new guidance affects your systems, processes, and internal controls. Project scoping may include or necessitate involvement from personnel involved in operations, internal controls, information technology, finance and tax. The company should consider compensation plans, debt agreements, tax matters and other areas in addition to company revenue contracts and business models.

In addition to the above, companies need to analyze where any changes will need to be made to IT system, software applications or processes in order to implement the new revenue recognition standard, including the retrospective adoption of the guidance. A full project plan including implementation of the standard and training of staff will need to be developed to manage the process, including plans for educating stakeholders such as the board of directors and investors. The team will need to determine the nature, timing and extent of work involved over the implementation transition timeline.

It is well advised to communicate frequently with your external auditor to ensure that your scoping is complete, and your implementation approach and the changes in accounting for revenue recognition are appropriate, and documented completely and accurately.

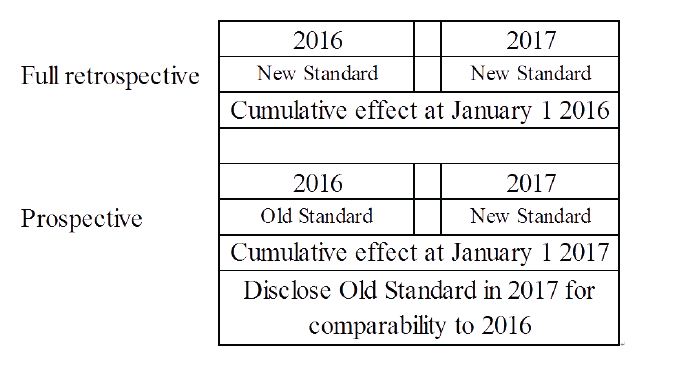

Determine transition method

As noted in Part I of our series on Revenue Recognition – there are two options under the guidance for retrospectively adopting the new revenue recognition standard:

Companies will need to determine which method is more appropriate and how to determine the accounting differences for the periods that require restatement.

Determine disclosures

Interim disclosures will need to be made including additional qualitative and quantitative disclosures over the impact of the retrospective adoption on the company’s financial statements, operations, how the company is doing the implementation and what, if any, significant changes to the internal control structure and reporting processes need to be made in order to implement the standard.

Implementation and Education

Initiate a performance monitoring scheme to collect the information needed to measure progress of implementation against the plan which was set. Training, education and follow up of implementation changes relating to the new revenue recognition standard will be key activities to ensure the adoption of the standard is successful. The project team should report to management, the audit committee and the board of directors periodically on progress to plan, issues encountered and solutions provided. The key stakeholders will need to understand what changes have been made in the timing of revenue recognition, the systems and processes surrounding revenue recognition and other changes resulting from the implementation of the new standard. Management should ensure open communication and information flow with the project team, management, key takeholders, internal auditors, and external auditors in order to ensure a successful transition to the new revenue recognition standard.

LehmanBrown can assist your company in the project management of implementing the new revenue recognition standard, whether it is under US GAAP or IFRS. Our team members have professional expertise in US GAAP, IFRS and PRC GAAP Accounting, as well as extensive experience in project management and compliance implementation projects.

To read Part 1 of this article, please click here.