Submission and Documentation for Transfer Pricing Report in China

Transfer pricing refers to the price set by affiliated enterprises when they sell goods, provide services and transfer intangible assets. In transnational economic activities, tax planning through transfer pricing among affiliated enterprises has become a common tax avoidance method or sometimes evasion. Because transfer pricing is not an exact science because of all of the considerations taken into account, it is also something that tax bureaus will review, and it has drawn more attention recently from the Chinese tax bureau.

The method involves enterprises in high-tax countries setting low prices when selling goods, providing services, and transferring intangible assets to affiliated enterprises in low-tax countries. Enterprises in low-tax countries set high prices when selling goods, provide services and transfer intangible assets to affiliated enterprises in high-tax countries. In this way, profits are transferred from high-tax countries to low-tax countries, minimizing their tax burden.

The Submission of Transfer Pricing Report

According to Article 43 of the Announcement of the Corporate Income Tax Law of the People’s Republic of China, the enterprise will attach the annual related party business dealings report for all business dealings between the enterprise and its associated parties when filing the annual corporate income tax returns. Where the tax authorities conduct investigations into the party business dealings, the enterprise, the related parties and other enterprises related to the related party business dealing under investigation will provide the relevant information according to the provisions.

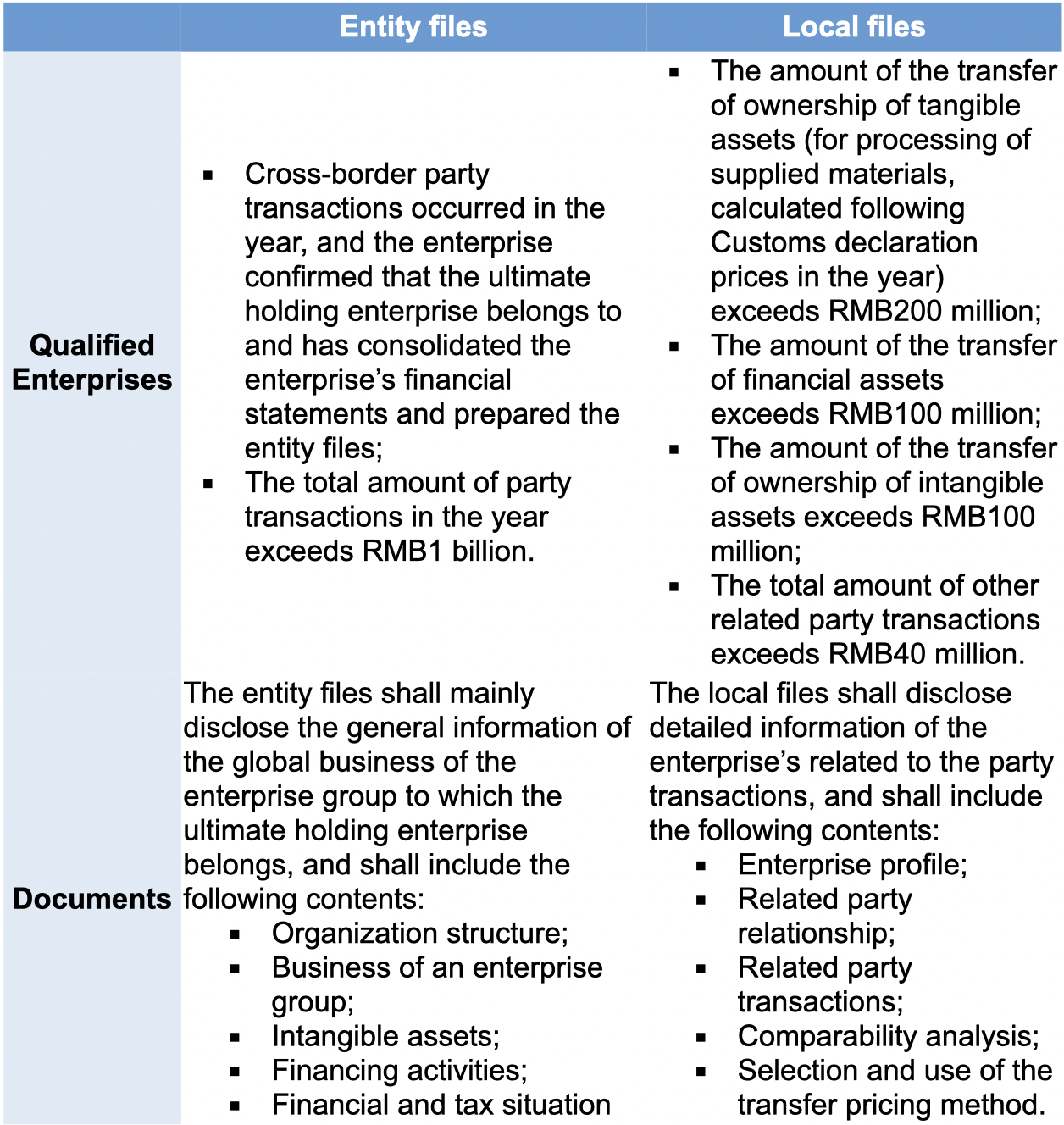

Documentation for Submission of the Transfer Pricing Report

According to Article 10 of the Announcement of the State Administration of Taxation on Matters Relating to Improved Administration of Related Party Declarations and Contemporaneous Documentation, an enterprise shall, according to the provisions of Article 114 of the Implementation Regulations for the Enterprise Income Tax Law, prepare the contemporaneous documentation for its related party transactions for the tax year and following the requirements of the tax authorities. Other documentation includes entity files, local files and special matter files.

Proactively Complying to Regulations

With the upgrading of China’s anti-tax avoidance laws and regulations, enterprises engaged in business or investment activities in China must actively manage transfer pricing risks and compliance requirements while paying more attention to the commercial purpose and substance of their operational framework. For multinational enterprises, it is necessary to consider appropriate tax and transfer pricing strategies to meet the requirements of tax laws and regulations, and prepare corresponding data as required. It is not only a requirement of compliance but also a useful tool for tax planning and risk management. It helps to prove that the related party transactions of the enterprises conform to the principle of independent transactions and the rationality of their business structure and arrangements.

Also, multinational enterprises must have a thorough understanding of the operations of the enterprises along with their functions, risks, assets and related costs, costs and profits to analyze the situation of related party transactions. From the prospect of transfer pricing, problems and dangers related to the party transactions must be identified and checked. Enterprises can formulate transfer pricing policies beforehand. It is also implemented in affiliated transactions to deal with possible investigations and audits by tax authorities.

Whilst only companies that meet the related party revenue criteria are required to file an annual transfer pricing report, all foreign companies operating in China are required to have completed an annual audit report undertaken by a Chinese CPA firm, and the notes section of the audit reports provide disclosures, and also the annual Corporate Income Tax filing also has a section for each related party transaction entity and nature. As such, it is important for all companies, large and small, to consider their transfer pricing policy, the risks, function reward for the entity in China, and the transfer pricing methodology used. It is also advisable for a comparable analysis to be prepared to justify the pricing methodology as within the middle quartiles of a standard mediation curve.

As transfer pricing is not an exact science, justification is arguability of the pricing and methodology used is the key to defending and tax department investigation.

How can LehmanBrown Help?

LehmanBrown has English speaking professionals who have assisted companies in evaluating their transfer pricing reports, review their documentation and identify any tax risks or any other potential issues. To discuss your business’ transfer pricing reports or any other concerns you are welcome to send your enquiry at enquiries@lehmanbrown.com.