Special Additional Deductions for Individual Income Tax Reform in the PRC

Please click here for the PDF version downloading.

According to the newly revised individual income tax law, for the calculation of taxable income of individual income in the future, besides the RMB5,000 tax exemption allowance and the special deduction such as “five insurances and one fund”, six special additional deductions will be added, such as children’s education, continuing education, medical treatment for serious diseases, housing loan interest, housing rent and expenditure for elderly dependents.

On 20th October 2018, the Ministry of Finance, the State Administration of Taxation (“SAT”) and other relevant departments jointly drafted the Interim Measures for Special Additional Deductions for Individual Income Tax (Draft), and put out to solicit public opinions for two weeks on the official websites of the two departments.

On 13th December 2018, the official Provisional Measures on Special Additional Deductions for Individual Income Tax was published and went into effect on 1st January 2019.

The Measure formulates the detailed scope, standards and implementation steps about the special additional deduction:

- How much can taxpayers save?

- How to deduct the special additional deductions?

- How to take the easy way out?

- The application of fringe benefits and special additional deduction for expatriates.

1. How much can taxpayers save?

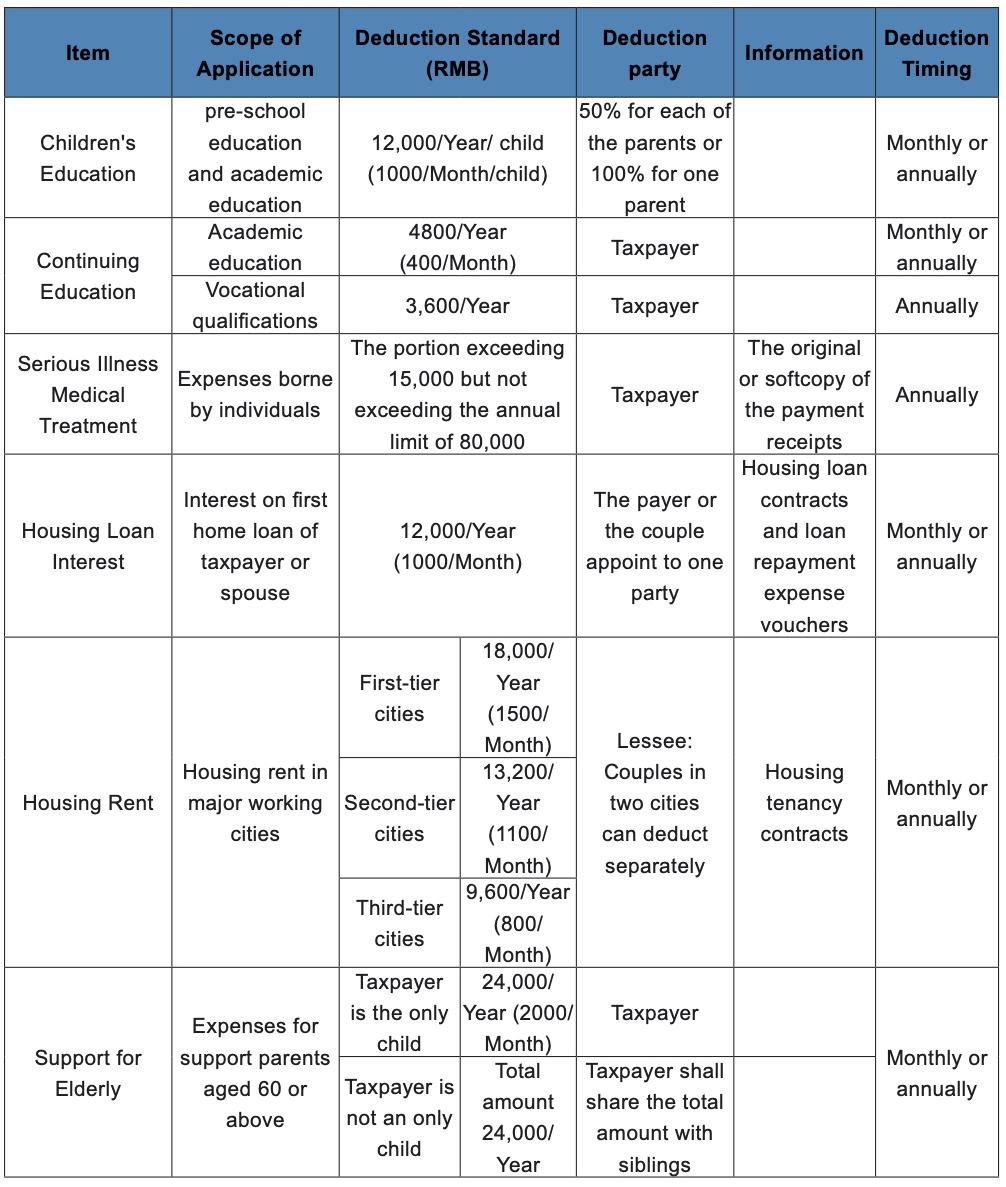

“Special additional deductions” refer to six types of special additional deductions, that is expenses for children’s education, continuing education, serious illness medical treatment, housing loan interest, housing rent and caring for elderly dependents as provided in the Individual Income Tax Law. This is the first time that the concept of special additional deduction is introduced into the individual income tax system in China. It is also widely regarded as an important step for China to carry out the individual income tax system combining synthesis and classification.

- Standards for deductions:

1.1. Children’s education expense

Standard deduction: Each child is RMB12,000 /year

This deduction includes the related expenditure of “pre-school education + academic education”. The pre-school education refers to the education from the age of three to primary school. The academic education including:

- Compulsory education: primary school and junior middle school education;

- Senior high school education: general senior high school and secondary vocational education

- Higher education: junior college, undergraduate, postgraduate and doctoral education.

In reference to “children”, it includes children born in wedlock, children born out of wedlock, step-children and adopted children.

1.2. Continuing education expense

Standard deduction: 4,800 yuan/year for academic education; RMB3,600 for skill education

Continuing education is another deduction, covering education carried out whilst a person is also working, such as studying an MBA or doctorate, and during the period of study a deduction of RMB4,800 /year, namely RMB400 /month can be enjoyed.

Another is to accept skills education, such as continued education for skills and professional qualifications. The scope of professional quantification is yet to be defined, but it is likely that it will be implemented according to the announcement of the national occupational qualification catalogue, a notice including a total of 140 items, covering teachers, engineers, accountants and other industries issued by the Ministry of Human Resources and Social Security.

1.3. Serious illness medical treatment

Actual deduction within the limit: RMB80,000 /year.

This deduction can greatly alleviate the burden of medical expenses for serious diseases of citizens, the provision of medical services can be deducted within the limit as long as the original or copy of the receipts related are provided.

The additional deduction is conditional on more than RMB15,000 being paid either on its own or outside the coverage under social insurance. Special additional deductions are only available for those with a starting point of RMB15,000 and those with maximum RMB80,000 per year.

1.4. Housing loan interest

Standard deduction: RMB1,000 /month

The expenses of housing loan interest of RMB12,000 per year during the repayment period, and only the loan repayment for the first property is qualified for the deduction. Commercial loans and provident fund loans are applicable to purchase a house for the taxpayer and his/her spouse.

1.5. Housing rent

Standard deduction of different levels depending upon city: RMB800-1,500 /month

This is the only item that has a regional difference.

On the premise that he/she does not own a house in the city he/she mainly works in, the rent expenditure incurred in the rental housing can be deducted according to the standard quota specified in the housing location of the rented housing:

- First-tier cities, which is a centrally-administered municipality, a provincial capital city, a city with independent planning status or any other city determined by the State Council, the standard quota for deduction shall be RMB18,000 per year (RMB1,500 per month);

- Second-tier cities, which is a city with a registered population of over 1 million in the municipal districts, the standard quota for deduction shall be RMB13,200 per year (RMB1,100 per month);

- Third-tier cities, which is a city with a registered population of not more than 1 million (inclusive) in the municipal districts, the standard quota for deduction shall be RMB9,600 per year (RMB800 per month).

1.6. Support for the aged

Standard quota: RMB2,000 /month

This is the highest amount of the special additional deductions. The deduction is RMB24,000 / year for those aged 60 or above, parents or other legal supported etc. The main premise is that no matter how many elderly are supported, the total quota is RMB24,000.

The total amount of deduction shall not exceed RMB24,000. For an only child, RMB24,000 can be deducted in full; If the taxpayer is not an only child, the deduction amount can be shared equally, specified by the elderly or apportionment agreed with sibling. Where the deduction amount is shared according to the apportionment, the taxpayer should sign a written agreement with sibling.

· Special additional deduction in calculation

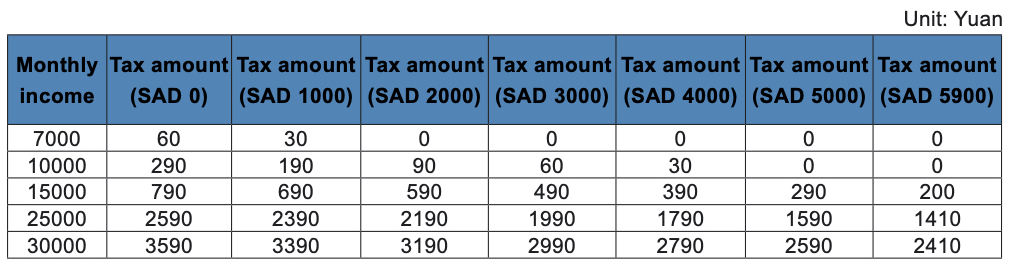

Except the additional deduction for medical treatment of serious diseases and other extremely special circumstances, it is assumed that one person conforms to the standard of four special additional deductions, namely enjoying the maximum deduction amount, the special additional deduction amount is calculated as follows in RMB: 1000 x 2 (children education) + 400 (continuing education) + 1500 (renting) + 2000 (support to elderly), totaling RMB5,900.

After the new tax law comes into effect next year, the income tax calculation method for the monthly income is as follows:

Taxable income = pre-tax monthly income – RMB5000 (standard deduction) – special deduction (social security and housing fund, etc.) – special additional deduction – other deduction determined by law.

On the basis of the above, an example of tax saving is:

For example:

Under each scenario the where taxable amount before the special additional deduction and special additional deduction are specified, the following table provides a summary for tax should be paid.

1. The Monthly income is the net amount of gross comprehensive income minus the deductible items (except special additional deduction).

2. SAD refer to special additional deduction

According to the table, we can find when the taxable income before the special additional is RMB30,000, the special additional deduction amount is RMB5,900, so RMB1,180 can be saved. It should be noted that, those that cannot be deducted in full in the current year shall not be carried forward to the next year for deduction.

2. How to deduct the special additional deductions?

So, what situations would qualify for the deduction? Regarding to items, contents, conditions and amount of deduction.

Per Chapter 8 in “Interim Measures for Special Additional Deductions for Individual Income Tax “, there are listed 10 categories of information, plus a “other information” catch-all clause. These can be summarized as follows:

Category 1: The deduction item under the standard deductions only requires to confirm the identity facts.

For example, the special additional deduction for supporting the elderly requires the only-child certificate issued by the health department and household registration information issued by the public security department. Children’s education special additional deduction needs the student status information of the education department; Housing rent special additional deduction needs to provide rental housing contract.

Category 2: The limited deduction items, only needs to prove the actual occurrence related expenditure data information.

For example, information about medical expenses borne by individuals by the medical protection departments, as well as the original or copy of the bill related to the medical service charge, can be used as the information of the special additional deduction for major illness medical treatment.

Category 3: The fixed deduction items, which needs both information of fact and actual expenditure proof.

For example, the real estate registration information of the real estate department, together with the repayment information provided by the housing provident fund center and the financial supervision department, can be used as the information of the housing loan interest special additional deduction. Continued education student status certificate, only with money collection receipts can be used as the information of continued education special additional deduction.

3. How are the deductions to work in practice?

· Information submission

To enjoy the deduction, relevant information needs to be submitted, including personal identity information of the taxpayer, spouse, minor children and the supported elderly. Taking full account of the convenience of taxpayers and the protection of privacy, there are two channels for submission: it can be submitted to the withholding agent or directly to the tax authorities.

· Information verification

Information will be consolidated between government departments, and personal information will be shared with the tax authorities. Relevant departments and organizations shall provide the tax authorities or assist to verify the following information related to the special additional deductions, including Public Security departments, Medical Protection departments, Civil Affairs departments, Diplomatic departments, the Supreme Court, educational departments, and other departments, the information will cover all aspects from healthcare to retirement, schools, real estate and marriage.

In the drafts and details provided so far, the tax authorities have not detailed much in the way of requirements for the supporting materials of the special additional deductions, in most cases the taxpayers are only required to keep the vouchers for reference.

Meanwhile, it requires the withholding agent to make withholding declaration according to the information provided by the taxpayer, which reflects the consideration of minimizing the burden on the taxpayer and the withholding agent. But it is also a test of taxpayers’ integrity, and tax authorities will also supervise through in various ways such as proportional random checks, cross-departmental information sharing, the use of taxpayers’ credit records and joint punishments.

If the taxpayer refuses to provide or provides fake credentials:

- for the first time, taxpayer and the withholding agent (the employer or someone who pays the salary) shall be bulletined / announced;

- If the situation is found again within five years, it shall be recorded in the taxpayer’s credit history, with joint punishment jointly imposed by relevant departments.

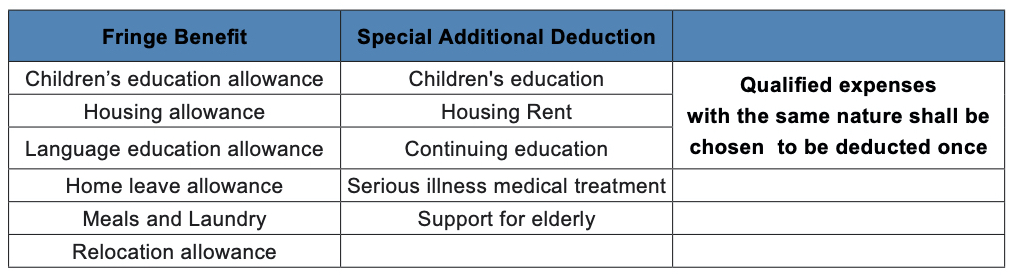

4. The application of fringe benefits and special additional deduction for expatriates

Some special additional deductions under the new tax law overlap with some of the fringe benefits under the current tax exemption, which also raises concerns about implementation of the tax exemption policy for foreign individuals. The Interim Measures clarifies the principle that a single expenditure shall not be entitled to two kinds of exemptions at the same time. Expatriates who meet the conditions for the deduction may choose one from the special additional deductions and the existing relevant subsidy exemptions.

Conclusion:

The introduction of special deductions is a huge step forward for China in both reducing the tax burden of individuals and also in providing support for those with children and aging parents and dependents. The implementation of the deductions and how these are supported, and the filing process still is to be clarified, but it is hoped that the eventual system is simple in its application and straight forward for its reporting.

There is also a question of how it might become inclusive of all, as if a person was located in the first-tier cities of Shanghai, Beijing, and Guangzhou, cannot afford to buy their first house, are living in a dormitories provided by their employer, has parents who are still young, has just completed a PHD and has no continuing education, is unmarried and has no children can benefit. Key to the implementation and ultimate enforcement of proper tax collection is going to be in the detail. For most people their employers have taken care of the tax filing and taxes due, where under the new system many more people are going to have to think about their taxes, and do annual tax filing taking into account their comprehensive income and deductions, which is going to require a lot of education.