How to Close a Company in China?

Closing a company in China can be complicated, and more so during Covid-19 and economic turmoil. China in the first quarter of 2020 saw many businesses registered in China come under financial stress, due to the added trade tensions and the global lockdowns caused by the pandemic. As shared on SCMP, the registration of new firms during the first quarter of 2020 compared to the year before fell by 29 per cent, and also about 460,000 Chinese firms shut during the first quarter, with some of these enterprises running for less than three years, or newer less established business. China businesses have since bounced back based upon domestic consumption and trade, however, the world economy still has a long way to go to recovery, which will affect many Chinese businesses still, as well as foreign businesses operating in China.

China has put in place a draft of policies to try and help businesses through these difficult times, focusing on the more vulnerable industries, saving jobs, and stimulating the economy.

Nonetheless, the fact remains that some companies may not survive, and in China, it is quite a complicated and time-consuming process to close a company as it mainly involves many different bureau and authorities, including:

- Tax Bureau;

- Customs;

- Bank and State Administration of Foreign Exchange (“SAFE”);

- Administration for Industry and Commerce (“AIC”);

- Social Welfare Bureau;

- Housing Fund Bureau; and

- Other special government depends on company nature.

Company Closing Procedures

Generally, the procedures for closing a company follows the following process outlined below:

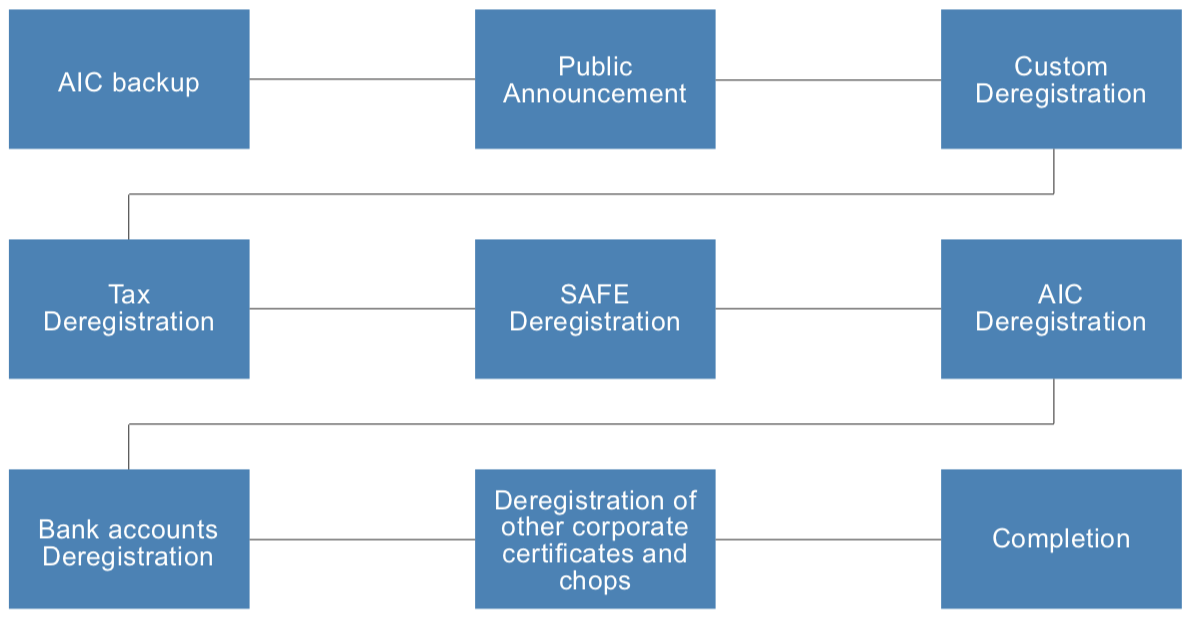

1. AIC Backup

AIC liquidation committee backup begins the whole deregistration process, and once approval is acquired, the company can arrange the deregistration public announcement. The claim declaration period is within 45 days after AIC backup. The creditors are requested to apply for creditor’s rights and debts during this period. If any issues occur or debts are not settled, the deregistration process cannot proceed.

2. Tax Deregistration

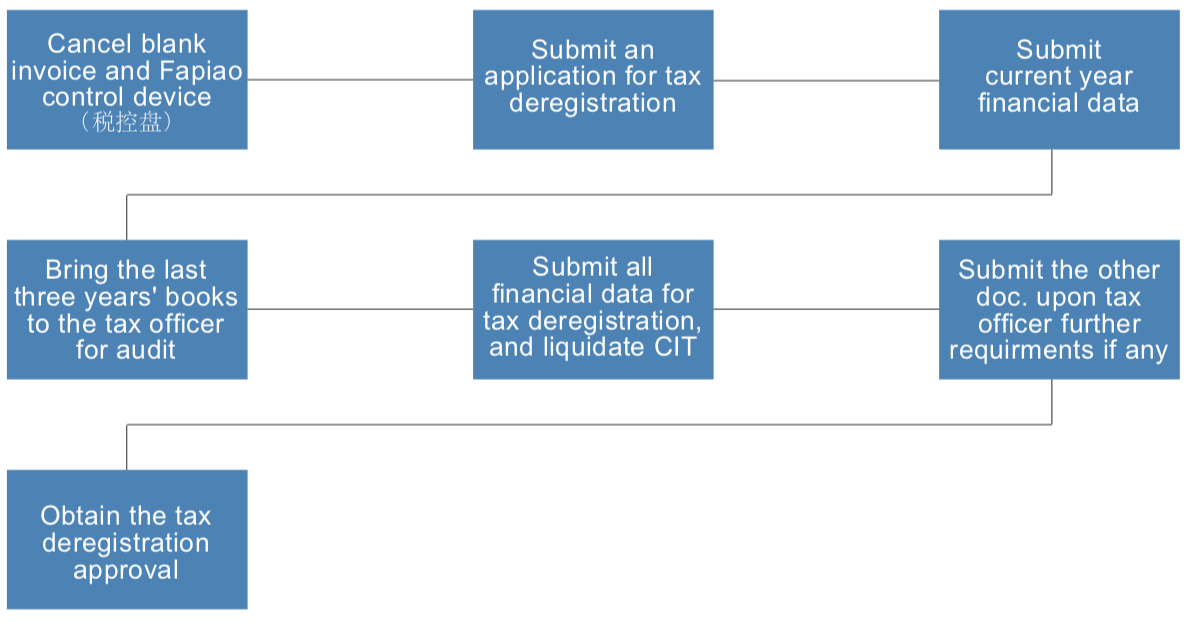

Tax deregistration requests the submission of necessary documents to the tax bureau from the past three years, and they can request a liquidation report, which is not too dissimilar to an audit report covering all of the years under review for closure clearance.

The tax deregistration process is as follows:

- Discussion with the tax officer regarding deregistration.

- Drafting the related documents upon confirmation with the in-charge officer.

- Deregistration of the fapiao control device.

- Submission of Application Letters.

- Completion of all financial data, including balance sheet and tax returns, profit and loss statement, etc.

- Submit the Audit reports for recent three years (only if applicable).

- Deliver all the required vouchers and accounting books to tax officers for review and their audit.

- Answer all questions or queries raised by the tax bureau.

- Other documents submissions on the officer’s further requirements.

- Collect the tax deregistration approval (clearance letters).

It normally takes between one and six months to complete the tax clearance, depending upon the tax office’s workload as well as the company financial status and if there are any tax issues found.

3. Other Certificates for Company Deregistration

For the other certificates’ deregistration which including AIC, customs, social welfare, housing fund and other bodies, the detailed procedures are as follows:

- Submission of Application Letters.

- Completion of all original application forms in Chinese and drafting the Board of Director’s minutes for deregistration.

- Submission of Application Letters to related bureaus.

- Answer all questions or queries raised by the bureau.

- Negotiate accordingly with the relevant Government Bureaus if there are any missing documents.

- Apply for the final approval from AIC with the related clearance letters mentioned above.

- Collect all the approvals (clearance letters) and the necessary documents from the Bureaus.

It normally will take between one and two months to complete the process.

4. SAFE report issuing and SAFE deregistration

Following the completion of the previous procedures, the next step in the process will be with the State Administration of Foreign Exchange (“SAFE”), for the completion of the following steps:

- Liquidation SAFE audit report issuance and preparation for the documents required. (takes between two and four weeks).

- Submit the filing package to the bank for initial review.

- If everything is fine with the bank, the bank will accept the filing package and hand over to its supervising bank branch for approval, or if not, they may request additional documents bank branches feedback.

- Once the bank approves the application, they will hand over to SAFE bureau for final approval.

The above will take between one and two months.

5. Closing the Bank

Bank accounts closure and fund transferring back to the parent of the closing company will need the following:

- Documents preparation and required data collection.

- General RMB bank account and its related e-banking cancellation.

- General USD bank account and its related E-banking cancellation.

- USD capital bank account clearance and money transfers.

- The balance in RMB from the basic bank account will remit to the investor and RMB bank account cancellation.

It will take between one and two months to finalize the bank accounts deregistration, and the processing time by the different banks will slightly differ, commonly the local banks will take longer than the foreign banks.

Other special certificates, license, organization deregistration documents, or services, which could be requested are:

Trade Union Deregistration

To facilitate the deregistration process the WFOE and the investor are required to apply for the Government bureaus below:

- Trade Union Committee

- Bank

- Chops

Other Special Certificates or License Deregistration

Tax clearance application

- Environmental or health and safety.

- Food operation License

- HR service license

- Dangerous Goods license

- Others

Common Pitfalls

Many common pitfalls can delay or hinder the proper closure of a company or Representative Office in China, including but not limited to, the following:

- Tax issues on fixed assets disposal, payable and receivable settlement, previous tax payment adjustment, missing invoices, etc.

- Employee issues such as labour disputes, salary and social welfare compensation etc.

- Legal suits with customs, suppliers etc.

- Unclear funds sitting in the bank account

- Customs clearance

In China, the deregistration process is quite complicated as it is also time-consuming. The process can take more than one year to complete, not including the time taken to handle any issues that are found during the process. Thus, it is always advisable to carry out a thorough review of the entity being closed to flush out any issues before starting the closure process. Where issues are close to the local management, it is advisable to have external professionals to help review the business to understand what issues may exist and to provide solutions to resolving these before or as part of the process of closure.

Establish a Plan

With a deeper understating of the procedures involved in deregistering a business in China, it is obvious why the recommendation is to plan and seek professionals to assist. COVID-19 has pushed China to innovate and allow some documents to be submitted online. The entry restrictions for foreigners has and continues to affect their ability to come to China to close the business’ bank accounts and sign off papers required to proceed to the next step of the process of closure. Solutions are available, however, the situation puts much risk to those registered as officers or in a formal capacity, especially for those who are the legal or chief representatives and are unable to have direct control.

Alternatively, it may be beneficial to have cashflow and audit reviews before considering deregistration and closure. Internal audits can assist businesses in any issues from past practices, such as tax, exposing human resources risks, reviewing business and directors’ risks before any application to close a business. At the same time, if a business has growing value within it, this could be quantified and the business possibly saved through some cost-cutting or a new strategy, or possible spin-off parts of the business or its assets or intellectual property. An external professional reviewing the business might find value internally overlooked by those in the business because of their closeness to the stressed situation.

To discuss your specific situation and find the best solutions do send your enquiry at enquiries@lehmanbrown.com.