The First Chinese Annual Advance Pricing Report Released

The State Administration of Taxation (“SAT”) issued the Chinese first annual advance pricing report (“APA”) titled “China Advance Pricing Arrangement Annual Report (2009) (“APA Report) on December 30, 2010. The groundbreaking report provides the official statistical survey on both in-progress and completed Advance Pricing Arrangements (APAs) for the period from January 1, 2005 to December 31, 2009 and reaffirm the SAT’s focus on transfer pricing issues, in particular, reinforces its commitment to the APA program. This report aims to provide a useful guidance to taxpayers, especially MNEs investing in China as well as Chinese enterprises with overseas investments that intend to adopt an APA. The information and insights provided by the report increases the transparency of the APA administration in China which is welcomed by the taxpayers.

Overview

The contents of the APA Report mainly include the following subjects:

- Introduction to China’s APA program;

- A history of the APA program’s development;

- The implementation procedures and related forms;

- Statistics on in-progress and completed APA cases; and

- Appendices of forms used in the APA application process.

APA procedures and process

Apart from the forms and procedural guidance previously released, the APA Report also contains new content including the statistics as well as a process flowchart detailing how an APA moves through the six phases, namely:

- Pre-filing meeting

- Formal application

- Examination and evaluation

- Negotiation

- Agreement and signing

- Execution and monitoring

The below flow chart illustrates the process:

Statistics

The APA Report provides a survey on the APA development in China since 2005 when the APA was formally incorporated under the corporate income tax law in China till the recent year of 2009.

The data released by the Report demonstrates a few key trends for the APA program in China which is summarized below:

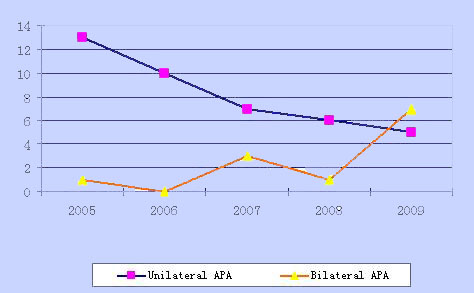

- 53 APAs in total has been signed during 2005 to 2009, among which the unilateral APA accounts for more than 77%. Nevertheless, the bilateral APA is growing rapidly and surpasses the number of the signed unilateral APA for the first time in 2009.

- As the end of 2009, no multilateral APA case has been concluded yet.

- The majority of the APAs concluded is related to purchase and sales of tangible assets as of the end of 2009. However, the application of APA involving intangible assets and services is increasing continuously and the number application in process has exceeded the application related to tangible transactions.

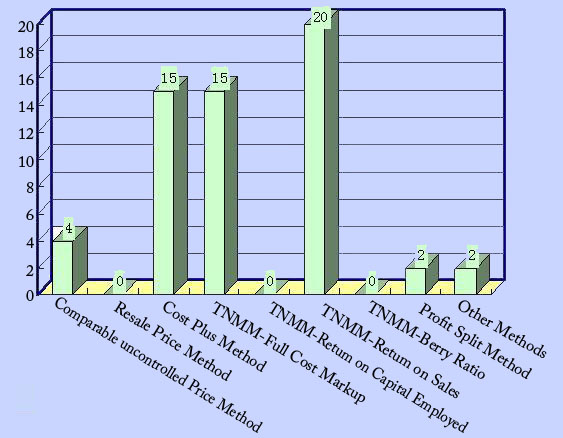

- The TNMM (transaction net margin method) is the most popular method adopted which accounts for 60% of the signed APA cases. Cost-plus is the second popular method whereby around 26% cases adopt it.

- The processing times for unilateral APA and bilateral APA application are becoming more expedited.

Below are the complete statistical data extracted from the APA Report:

| Table 1: Number of APAs Signed | ||||

| Year | Unilateral APAs | Bilateral APAs | Multilateral APAs | Total |

| 2005 | 13 | 1 | 0 | 14 |

| 2006 | 10 | 0 | 0 | 10 |

| 2007 | 7 | 3 | 0 | 10 |

| 2008 | 6 | 1 | 0 | 7 |

| 2009 | 5 | 7 | 0 | 12 |

| Total | 41 | 12 | 0 | 53 |

| Table 2: APAs by Phase (as of December 2009) | ||||

| Phases | Unilateral | Bilateral | Total | |

| Pre-Acceptance | Proposal/letter of intent | 0 | 20 | 20 |

| Pre-filing meeting | 26 | 5 | 31 | |

| Accepted | Examination and evaluation | 0 | 5 | 5 |

| Negotiation | 2 | 8 | 10 | |

| Subtotal | 2 | 13 | 15 | |

| Concluded APAs | Agreed but not signed | 0 | 1 | 1 |

| Executed and Monitored | 18 | 11 | 29 | |

| Expired | 23 | 1 | 24 | |

| subtotal | 41 | 13 | 54 | |

| Total | 69 | 51 | 120 | |

| Table 3: APA by Transaction Type | |||||

| Accepted Application | Concluded APAs | ||||

| Transaction Type | Number of APAs | Percentage | Transaction Type | Number of APAs | Percentage |

| Purchase and sale of tangible assets | 11 | 46% | Purchase and sale of tangible assets | 42 | 62% |

| Transfer or use of intangible assets | 8 | 33% | Transfer or use of intangible assets | 13 | 19% |

| Provision of services | 5 | 21% | Provision of services | 13 | 19% |

| Financing | 0 | – | Financing | 0 | – |

| Total | 24 | 100% | Total | 68 | 100% |

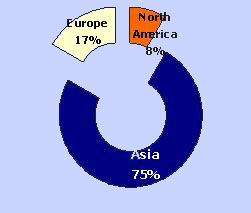

| Table 4 : Bilateral APAs, by Region of Counter-party | |

| Region | Signed APAs |

| Asia | 9 |

| Europe | 2 |

| North America | 1 |

| Total | 12 |

| Table 5: APA by Processing Time | |||||

| Type | Processing Time from application to Signing | ||||

| <1 Year | 1-2 years | 2-3years | > 3 years | Total | |

| Unilateral | 23 | 18 | 0 | 0 | 41 |

| Bilateral | 7 | 3 | 1 | 1 | 12 |

| Table 6: APAs by transfer pricing method

|

Our observations

APA program is viewed by SAT as an effective method to provide certainty for both the tax authorities and tax payers in regards to transfer pricing issues which is beneficial to both parties. On one hand, APA reduces the compliance costs for tax payer by mitigating the transfer pricing audit risks, avoiding the double taxation risks under bilateral / multilateral APA, providing higher assurance to the cross border operations. On the other hand, APA help to save administration costs for tax authorities in respect of transfer pricing issues, providing expectation of stable revenue.

This Report clearly demonstrates that SAT supports APA developments in China. More effort and resources shall be expected from SAT for improving the related APA administration in China, moving towards the international standard and practice, building up a transparent system, adopting the technically advanced APA approach.

Meanwhile, we also observed that SAT becomes more and more selective in accepting the APA applications. The reason behind is believed as that SAT aims to set precedents for transfer pricing for the same industries for the whole country through APA exercise. As a result, for certain industries the acceptance rate of the application may be affected.

The APA mechanism has been proved a useful tool for resolving transfer pricing issues, it is an important risk management tools for multinational enterprises (MNEs), those MNEs shall be aware of the new trend and practice developments in China so as to assess the risk and opportunities in a dynamic regulatory environment.