Final Stage of Business Tax to VAT (“B2V”) Reform

On 5th March, 2016, Premier Li Keqiang announced at the opening of the National People’s Congress that the real estate and construction, financial services and insurance, and lifestyle services industries will all be subject to VAT with effect from the 1st May 2016. This signifies the completion of the B2V reform measures within this year. China’s indirect tax system introduced in 1994 comprising of both VAT and BT will now become obsolete.

The completion of B2V reform is expected to bring in a series of changes on VAT policy and administration which will have a profound impact on all businesses in China.

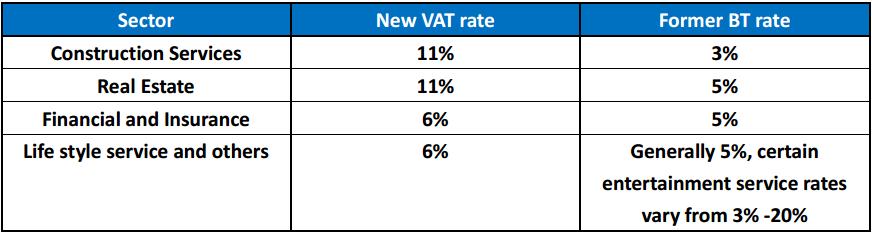

The VAT rates applied to the respective industries and a comparison with the current BT rates are set out below:

For those meeting the requirements, the General VAT payer is effectively assessed on a net basis (VAT Payable = Output VAT – Input VAT) while BT is assessed on a gross basis, a straight comparison between the new and the old rates is not valid. For those not meeting the requirements of General VAT, these companies would be classified as a Small Scale VAT payer, and would be paying taxes on the revenue with no offset for input VAT, but with a lower VAT rate at 3% which is reduced from the former BT rate of 5%.

The timeframe for implementation of around 5-6 weeks from the release date of the new rules will be very challenging for businesses to meet. It is expected that many companies which are not already well prepared will face some challenges and uncertainties.

To be better prepared for the upcoming 1st May reforms, you may consider the following:

Tax Impact Analysis:

Review of operation modes, structure of taxes and expenses, investigation of suppliers for their tax status and ability to provide proper tax receipts etc.

Contract Review:

Review tax related clauses for old contracts and develop standard clauses post – reform to reflect the new tax position.

System Updates

Enhance the VAT risk and invoice controls, update the accounting requirements, chart of accounts and internal processes and procedures for VAT.

Training

Internal and external training to personnel not only in the tax and finance departments, but across other relevant departments.