Audit Requirements for Foreign Invested Companies in China

Please click here for the PDF version downloading.

Background

As the world’s second largest economy, China has attracted a large amount of foreign capital to conduct business in China through the establishment of foreign-invested companies. In view of the current complex and sophisticated investment environment in China, the supervision of foreign investment by local governments is becoming much stricter.

In order to track the financial performance of these companies, foreign invested companies are required to submit audited financial statements to related authorities for annual inspection and tax filing.

In addition to the statutory requirement, the need for companies’ financial statements to be audited by an independent external auditor has been a cornerstone in a world’s financial systems. With the separation of ownership and management rights, the owners no longer need to participate in the daily operation and company management, which produces the problem of how the owners know and control the behavior of the operator. Thus, the operator needs to report the financial status and operating results to the owners periodically through the financial statements. The annual audit report or quarterly and monthly reporting could well help to report the financial position and performance to the owners.

This article illustrates what a proper financial statement audit entails and the value and how it can benefit businesses in China.

Definition of financial statement audit

In general, an audit consists of evaluation of subject matter with a view to expressing an opinion on whether the subject matter is fairly presented.

As for financial statements audit, audits are undertaken to form an independent opinion on the financial statements of a company to assure whether the financial statements are free from material misstatements.

Materiality is a concept used by both preparers and auditors of financial statements to help determine what information is important, what information should be disclosed in the financial statements, and to evaluate misstatements.

Information is material if its omission or misstatement could influence the economic decisions of users taken on the basis of the financial statements. Materiality depends on the size and nature of the item or error judged in the particular circumstances of its omission or misstatements. When determining whether a matter is material, the auditors also evaluate qualitative considerations, such as the impact of misstatements on debt covenants, key ratios, etc.

Purpose of a financial statement audit

Companies produce financial statements that provide information about their financial position and performance. This information is used by a wide range of stakeholders in making business decisions. Typically, the owners or the shareholders of a company are not executives. Therefore, the owners of these companies take comfort from independent assurance that financial statements fairly present, in all material respects, the company’s financial position and performance for a specific historical period.

To enhance the degree of confidence in the financial statements, a qualified external party (an audit firm) is engaged to audit the financial statements, including related information disclosed by management, to give their professional opinions on whether they fairly present, in all material respects, the company’s financial performance over a given periods and financial position as of a particular date in accordance with relevant General Accepted Accounting Principles (“GAAP”), known as Accounting Standards for Business Enterprise (“PRC GAAP”) in China.

In addition, an audit of financial statements is required as a statutory requirements. In China, the statutory requirement is that the Foreign Invested Company (“the FIC”) is required to submit its audited financial statements to related authorities for annual reporting and tax filing. The related authority would mainly focus on whether financial statements comply with PRC GAAP, local tax regulations and etc. A proper financial statement audit would help the company avoid the risk of any violations in these regulations.

Benefits of a financial statement audit

Not only the financial statement audit mainly focuses on the assurance of compliance with applicable reporting standards, there are important additional value aspects of the audit process. A rigorous audit process will, almost invariably, also identify insights about some areas where management may improve their controls or processes. In certain circumstances the auditor may be required to communicate control weakness to management and those charged with governance. These communications add value to the company and enhance the overall quality of business process. Audit issues as such involved in these communications would be reported to the management and the directors of the company through annual audit report together with management letter (if necessary) which lists the audit issues or weaknesses identified and related recommendations.

How fraud affects financial statement audit

Fraud has a corrosive effect on the trust necessary for companies to do business. Management is responsible for running the company and preventing and detecting fraud. Preventing and detecting fraud is difficult because fraud is internationally hidden and may involve collusion by multiple participants.

Even though audits are properly performed in accordance with relevant auditing standards, they may not detect material fraud. However, auditors are responsible for obtaining reasonable assurance that the financial statements are not materially misstated as a result of fraud.

Importantly however, if the auditors form suspicions of fraud in the course of their work a number of things will change, including their risk assessment (see below), the nature and extent of communications with those charged with governance, and the evaluation of the effectiveness of the relevant internal controls and processes. The knowledge that an independent external audit will be conducted generally has a deterrent effect against fraud.

What a proper annual audit entails

Broadly, the audit process can be summarized in five phases:

Planning – Initial planning activities include formal acceptance of the client by the audit firm, verifying compliance with independence requirements, building the audit team and performing other procedures to determine the nature, timing and extent of procedures to be performed in order to conduct the audit in an effective manner.

Risk assessment – Auditors use their knowledge of the business, the industry and the environment in which the company operates to identify and assess the risks that could lead to a material misstatement in the financial statements. Those risks often involve a high degree of judgment and require a significant level of knowledge and experience by the auditor, particularly on large and complex engagements. This requires a good understanding of the business and its risks, which is typically built up over a number of years as part of the audit firm’s and auditor’s knowledge. It also means that the auditors need to be well informed about the industry and the wider environment in which the company operates, and about what its competitors, customers, suppliers and where relevant-regulators are doing.

Audit strategy and plan – Once the risks have been assessed, auditors develop an overall audit strategy and a detailed audit plan to address the risks of material misstatement in the financial statements. Among other things, this includes designing a testing approach to various financial statement items, deciding whether and how much to rely on the company’s internal controls, developing a detailed timetable, and allocating tasks to the audit team members. This audit strategy and plan are continually reassessed and adjusted to respond to new information obtained about the business and its environment throughout the audit process.

Detailed processes involved in the first three procedures can be shown graphically as follows.

Gathering evidence – Auditors apply professional skepticism and judgment when gathering and evaluating evidence through a combination of testing the company’s internal control, tracing the amounts and disclosures included in the financial statements to the company’s supporting books and records, and obtaining external third party documentation. This includes testing and management’s material representations and the assumptions they used in preparing their financial statements. Independent confirmation may be sought for certain material balances such as cash.

Normally, procedures conducted by auditors in the process of gathering evidence are controls testing and substantive testing.

(1) Controls testing

As businesses have grown more complex and sophisticated, and the costs of labor have risen, automated systems and processes have necessarily become much more prevalent. A well-run business will have its own systems and controls in place to operate efficiently, safeguard its assets, and to provide reasonable and assurance that its transactions are properly reported and that its financial statements are complete and accurate. The auditors assess the effectiveness of these controls in preventing and mitigating the possible risk of material misstatement in those areas where the auditor plans to use such controls to adjust the nature, timing and extent of their testing. If they believe the controls are effective, and they have tested that they operated reliably throughout the year, then the level of substantive audit evidence needed to give an opinion may be reduced. Even if the controls are reliable, varying degrees of substantive audit evidence will still always need to be gathered.

(2) Substantive testing

In addition to testing controls, the auditors is required to perform further procedures to gather evidence from substantive procedures, which can include a combination of the following:

- Physically observing or inspecting assets (such as inventory or property, plant and equipment);

- Examining records to support balances and transactions;

- Obtaining confirmations from third parties the company does business with (such as its suppliers, customers and in particular the banks it uses);

- Checking elements of the financial statements by comparison to relevant external information and investigating any differences (for example, using an external market index to check pricing and valuations);

- Checking calculations.

Details process involved in the procedure of gathering evidence can be shown graphically as follows.

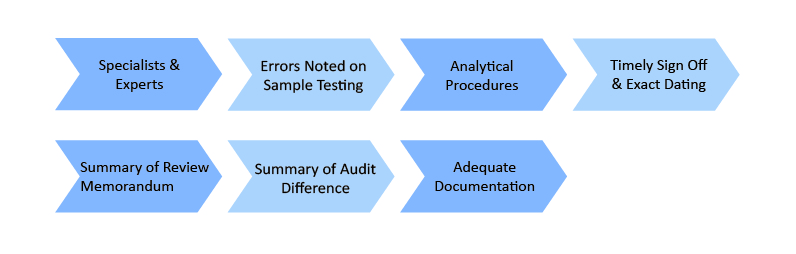

Finalization – Finally, the auditors exercise professional judgment and form their overall conclusion, based on the tests they have carried out, the evidence they have obtained and the other work they have done. This conclusion forms the basis of the audit opinion.

Auditors interact with the company during all the phases of the audit process listed above. There will be continuing discussions and meeting with management, both at operational and senior executive levels, and with those charged with governance. Using their professional skepticism and judgment, auditors challenge management’s assertions regarding the numbers and disclosures in the financial statements.

Details process involved in the procedure of finalization can be shown graphically as follows.

How we can help

LehmanBrown is a licensed China-focused accounting, auditing, taxation and business advisory firm, operating in Beijing, Shanghai, Hong Kong, Macau, Shenzhen, Guangzhou and Tianjin. The firm also manages an extensive affiliate network, providing service throughout China.

We have rich experience in audit service for FIEs, and offer comprehensive audit services for both local and overseas reporting requirements including restatement of financial accounts for Generally Accepted Accounting Principles (GAAP), International Financial Reporting Standards (IFRS), US GAAP compliance, China Statutory Audit, Hong Kong Statutory Audit and other special audits as requested.

Any enquiries, please contact LehmanBrown by enquiries@lehmanbrown.com

LehmanBrown International Accountants is a licensed China-focused accounting, taxation and business advisory firm, operating dedicated offices in Beijing, Tianjin, Shanghai, Shenzhen, Guangzhou, Hong Kong and Macau, and with an extensive affiliate network throughout China and in over 100 countries worldwide.