Administrative Measures on Accounting Records

Please click here for the PDF version downloading.

The Administrative Measures on Accounting Records (“the Measures”) were revised and adopted by the ministerial meeting of the Ministry of Finance and the National Archives Bureau in 2015. The Measures became effective on the 1st of January 2016. This article will focus on the adjustments made, and in particular what accounting records need to be maintained by companies, in what format, and for how long. Failure by companies to follow the rules can lead to serious legal consequences to the legal representative, the directors, and the accountants, also seriously hinder the company in the future. Additionally, there is a draft legislation being put in place regarding the responsibilities of accountants and consequences for improper accounting, which from 2020, China intends to roll out with the Corporate Social Credit System.

The revised Measures made adjustments to the following aspects:

– Refine the definition and scope of accounting files

The Measures defines the accounting records as “various forms of accounting materials such as text and tables, which are received or formed in the accounting process of the organisation, recording and reflecting the economic business matters of an organisation and worthy of preservation, including electronic accounting records formed, transmitted and stored through electronic equipment such as a computer.”

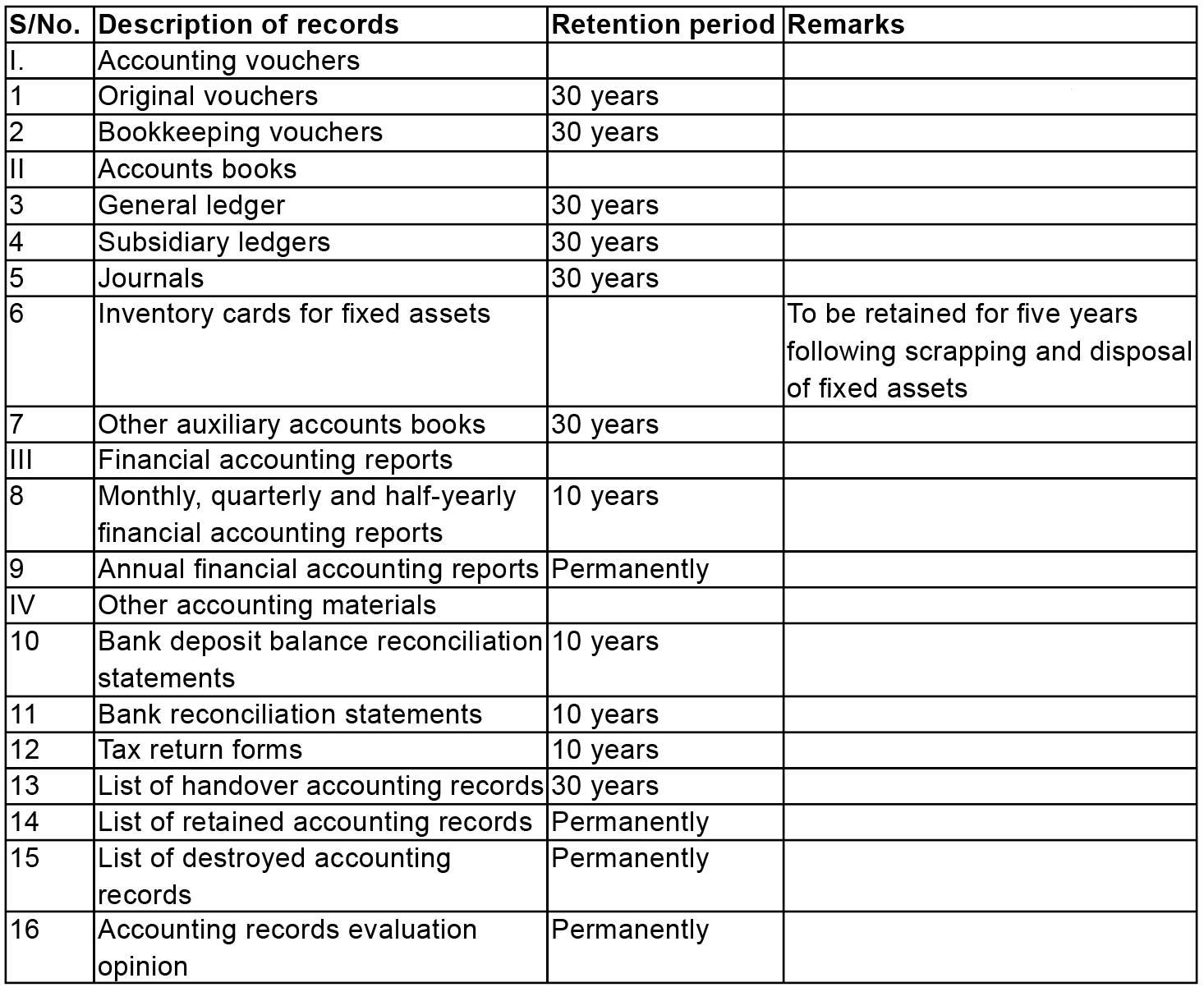

The Measures requires the following documents should be filed:

- accounting vouchers, including original vouchers and bookkeeping voucher

- account books, including general ledger, subsidiary ledgers, journals, inventory cards for fixed assets and other auxiliary account books;

- financial accounting reports, including monthly, quarterly, half-yearly and annual financial accounting reports;

- other accounting materials, including bank deposit balance reconciliation statements, bank reconciliation statements, tax return forms, list of handover accounting records, list of retained accounting records, list of destroyed accounting records, accounting records evaluation opinion and other accounting materials worthy of preservation.

-Clarify the requirements for the administration of electronic accounting files.

Organisations may use information technology, such as computers and network communications, to manage their accounting records. For any financial record generated internally, if the following criteria are all met, it may be kept only in electronic form and create the electronic accounting files.

- the source of electronic accounting materials formed are accurate and fair, and are created and transferred via electronic equipment such as a computer;

- the accounting system the company uses must be able to receive and process the data accurately, completely and effectively. It also has to be able to produce the accounting vouchers and financial statements that meet the national standards. It also has to reflect the procedures of the making and approving of the accounting records;

- the accounting files management system should be able to receive, manage and utilise electronic accounting records effectively. It also has to meet the need for long-term management of the accounting files. Referencing should be established between the electronic accounting records and the hard copy accounting files;

- the management system can effectively prevent accounting records from being tampered with;

- the backup system for accounting records should be made in case of natural disasters, accidents and vandalism;

- the accounting files are not the ones which are worthy of permanent preservation or possess significant preservation value.

Where the criteria stated above are satisfied, the electronic accounting materials received by an organisation from external sources and affixed with an electronic signature which complies with the provisions of the Electronic Signature Law of the People’s Republic of China may be archived electronically and hold electronic accounting records.

-Adjust the regular maintenance period of accounting files and extend the period for transferring the accounting files.

Accounting records formed within the current year may, at the end of the accounting year, be retained temporarily by the accounting management department of the organisation for a year before handing over the organisation’s archive management department or outside archive storage provider for retention. Where there is a need to defer handover due to work requirements, the consent of the organisation’s archive management department is required. The regulation does not explicitly advise what it means by archive management department, but in practice, it is designed to ensure the safekeeping of records by the company, controlled by senior management/officers of the company.

The temporary retention period of accounting records by the organisation’s accounting management department shall not exceed three years. During the temporary retention period, retention of accounting records shall comply with the relevant provisions of the State on the administration of archives. The cashier personnel shall not take on the task of retention of accounting records concurrently.

The retention period of accounting records shall be classified into two categories, permanent and fixed-term. Fixed-term retention period shall generally be 10 years and 30 years. Which is significantly longer than most countries, and it is important to note, as when a company is being reviewed, e.g. transfer pricing, the tax authorities can go back 10 years, or if suspected fraud, longer.

The retention period of accounting records shall start on the first day following the end of the accounting year.

The revised Measures also provide appendices of the retention period for different types of accounting records. In this article, considering the nature of the clients of the LehmanBrown, we will focus on the retention period for commercial companies and other organisation.

Appendix 1: Retention Period for Accounting Records of Enterprises and Other Organisations

-Refine the procedures for destroying accounting files

An organisation shall regularly evaluate accounting records for which the retention period has expired, and formulate accounting records evaluation opinion. Upon evaluation, where it is necessary to continue retention, retention period shall be re-determined for the accounting records. Accounting records which do not have preservation value upon expiry of their retention period may be destroyed.

The archive administration department of an organisation shall take the lead for evaluation of accounting records, and organise the accounting, audit and disciplinary supervision departments or personnel thereof to carry out the evaluation jointly.

Upon evaluation, accounting records which can be destroyed shall be destroyed in accordance with the following procedures:

- the archive administration department of the organisation shall formulate a list of destroyed accounting records, setting out the description of destroyed accounting records, file numbers, number of volumes, year of commencement and termination, archive serial number, retention period, retained period and date of destruction etc.

- the person-in-charge of the organisation, the person-in-charge of the archive administration department, the person-in-charge of the accounting management department, the handling officer of the archive management department, and the handling officer of the accounting management department shall sign on the list of destroyed accounting records.

- the archive management department of the organisation shall be responsible for organising the destruction of accounting records, and assign personnel jointly with the accounting management department to supervise the destruction. The supervising staff shall, before the destruction of the accounting records, compare and verify against the contents listed in the list of destroyed accounting records; upon the destruction of accounting records, the supervising staff shall sign or affix the seal on the list of destroyed accounting records.

Destruction of electronic accounting records shall also comply with the provisions of the State on electronic records, and the archive management department, accounting management department and information system management department of the organisation shall assign personnel jointly to supervise destruction.

Accounting vouchers for debts and creditor’s rights which are unsettled upon expiry of the retention period and accounting vouchers for other pending matters shall not be destroyed. The hard copy accounting records shall be retrieved and filed separately, and the electronic accounting records shall be carried forward separately for retention until the pending matters are settled.

Accounting records retrieved and filed separately or carried forward separately shall be stated in the accounting records evaluation, the list of destroyed accounting records and the list of retained accounting records.

Where an organisation is revoked, dissolved, bankrupt or otherwise terminated, the accounting records formed before termination or completion of deregistration formalities shall be kept by the archive department of the organisation, or an organisation which satisfies archive management criteria to manage the accounting records on its behalf. The retention period for those records is the same as the period illustrated in the form above.

-Transferring accounting records

At the time of handover of accounting records, both parties shall complete the handover formalities for accounting records.

The organisation handing over the accounting records shall formulate a list of handover accounting records, setting out the description of handover accounting records, file number, number of volumes, year of commencement and termination, archive serial number, retention period, retained period etc.

At the time of handover of accounting records, both parties shall hand over every item based on the list of handover accounting records, and the relevant person(s)-in-charge of both parties shall be responsible for supervision. Upon completion of the handover, the handling officers and supervising personnel of both parties shall sign or affix the seal on the list of handover accounting records.

Electronic accounting records shall be handed over together with the metadata, and electronic accounting records in special format shall be handed over along with the accessible platform. The organisation receiving the records shall inspect the medium and technical environment of the retained electronic accounting records, and ensure the veracity, integrity, availability and security of the electronic accounting records received.

An organisation which entrusts an intermediary to carry out bookkeeping shall specify the management requirements for accounting records and the corresponding responsibilities in the written entrustment contract signed between the organisation and the intermediary. Companies should ensure that their outsource provider maintains proper records on their behalf, and an agreed archive policy should be put in place.

Any enquiries, please contact LehmanBrown by enquiries@lehmanbrown.com

LehmanBrown International Accountants is a licensed China-focused accounting, taxation and business advisory firm, operating dedicated offices in Beijing, Tianjin, Shanghai, Shenzhen, Guangzhou, Hong Kong and Macau, and with an extensive affiliate network throughout China and in over 100 countries worldwide.